Thiruvananthapuram, Mar 13: Kerala Assembly on Friday witnessed unprecedented and ugly scenes as Finance Minister K.M. Mani, facing allegations in the bar bribery issue, presented the state budget amdist stiff resistance by LDF-led Opposition who tried all means to thwart his attempt.

The protest siege of LDF and Yuva Morcha activists outside the Assembly also turned violent. The protesters hurled stones at police and they in turn used teargas shells.

With the LDF making it clear that all roads leading to the Assembly would be blocked, Mani and some of his colleagues stayed back in the Assembly complex since Thursday’s session.

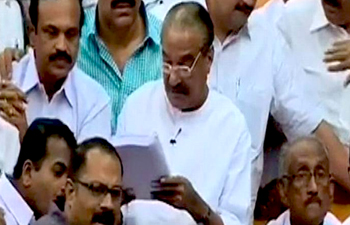

Mr. Mani, who managed to enter the Assembly amidst bedlam, read out some excerpts of the budget in the guard of watch and wards and tabled it before the House.

Members of LDF-led opposition, who were stressing their demand for resignation of Mr. Mani over the bar bribery issue, also stayed back in the Assembly after Thursday’s session and sat in the well of the House since morning.

Opposition MLAs, including senior leaders and women members, were adamant in their stand that they would not allow the “tainted” minister to present the budget.

They also laid siege at the entrance of the Assembly hall to check Mr. Mani from entering there. However, the ruling MLAs managed to bring the 82-year-old Finance Minister in the hall.

There was also a scuffle between the opposition members and watch and wards.

Meanwhile, a group of LDF MLAs rushed to the Speaker’s dais and threw his chair out of podium.

The CPI(M) MLA V Shivankutty, who felt uneasiness amidst the chaos, was given first-aid.

Vigilance and Anti-Corruption Bureau had registered a case against Mani in December last year in connection with the allegations that he had accepted bribe from bar owners to renew liquor licences.

The allegations were levelled by Kerala Bar Hotel Owner’s Association Working president Biju Ramesh.

Comments

Add new comment