New Delhi, June 2: Bihar, which was synonymous with poverty, has emerged as the fastest growing state for the second year running, clocking a scorching 13.1% growth in 2011-12. Not just that, on the back of four years of double-digit growth, its economy is now bigger than that of Punjab—until recently the preferred destination of Bihari migrant workers.

New Delhi, June 2: Bihar, which was synonymous with poverty, has emerged as the fastest growing state for the second year running, clocking a scorching 13.1% growth in 2011-12. Not just that, on the back of four years of double-digit growth, its economy is now bigger than that of Punjab—until recently the preferred destination of Bihari migrant workers.

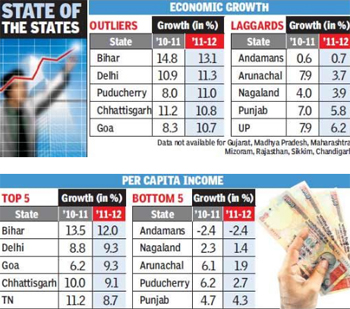

Among the top five states, Bihar is followed by Delhi and Puducherry. Mineral-rich Chhattisgarh, which many had written off for the violent Naxal movement, and Goa complete the top five growth listings, according to data available with the ministry of statistics.

Gujarat—a favoured destination for investors, both domestic and foreign—is again out of the reckoning for the top five slots, expanding 9.1% during the last financial year, according to data submitted to the Planning Commission on Friday. Among the more industrialized states, only Tamil Nadu was ahead of Gujarat with 9.4% growth (at 2004-05 prices).

Punjab, known as the grain bowl of India, Andhra Pradesh and Karnataka, both IT hubs, and Uttar Pradesh, the country's most populous state, clocked growth that was lower than India's GDP growth of 6.5% in 2011-12.

Economists, however, said that 9% growth by some of the larger states such as Gujarat and Tamil Nadu was credible given that they were growing on a much larger base.

In comparison, states such as Bihar and Chhattisgarh had a much lower base. For instance, at 2004-05 prices, economic activity in Tamil Nadu's was estimated at Rs 4.28 lakh crore, the highest among states for which data is available with the Central Statistics Office (CSO), while Bihar's gross state domestic product (GSDP) at 2004-05 prices was estimated at Rs 1.63 lakh crore.

In fact, Tamil Nadu beat Uttar Pradesh as the second largest state economy, after Maharashtra. UP's economy was estimated to be worth Rs 4.19 lakh crore in 2011-12, while Maharashtra, for which data is unavailable, is expected to retain its number one slot given that its economy was worth over Rs 7 lakh crore in 2010-11. In recent years, Maharashtra has lost out on investment to states such as Gujarat and Tamil Nadu and growth has slowed.

With the Bihar government taking up road building and other construction work in a big way, and with the state's law and order situation improving, consumers who were earlier wary of flaunting their wealth are now buying cars and bikes at an unprecedented pace. Rural demand too has got a boost with agricultural productivity rising for several crops, and with an improvement in connectivity and state-funded programmes for education, health and livelihood. Bihar is currently among the fastest growing markets for tractors.

"There are two things happening in Bihar. One, investment sentiment has picked up largely because of governance issues. Two, Bihar's growth is against a very low base. But there is a lesson in it for others," said N R Bhanumurthy, professor at the National Institute of Public Finance & Policy.

"States with internal demand will do better while those that are dependent on corporate demand tend to perform relatively worse at a time when corporate investments are low," added Pronab Sen, principal advisor in the Planning Commission and a former chief statistician.

Incidentally, data for Madhya Pradesh and Rajasthan, which made up what were once the Bimaru states, was unavailable.

Comments

Add new comment